25,000 Insured Ethiopian Farmers Receive Payments for El Niño Droughts

A farmer in Shehoch Tehara village in Amhara, Ethiopia, November 2014. Photo by Bristol Mann/IRI

More than 25,000 insured farming families in Ethiopia have received payments for crop loss and damages after a year of devastating drought caused in large part by the 2015 El Niño. The farmers purchased the insurance through the R4 Rural Resilience Initiative [latest report], run by the World Food Program and Oxfam America.

Since R4’s inception in 2011, IRI has been providing the climate and technical expertise to design the program’s index insurance, which is based on satellite rainfall measurements. These measurements are converted into a rainfall ‘index’ that determine if payments happen.

The rainfall measurements we saw at the beginning of the season, when farmers needed to plant, were some of the lowest on record. Our team has never seen anything like it.

The drought in Ethiopia highlights a new challenge confronting the index insurance community right now, a shift from a focus on the technology to one that builds the package most useful for a farmer, given a very tight insurance payout budget.

Concepts like basis risk–the gap between the losses farmers have and the losses covered by insurance payouts–need to be re-thought. In Ethiopia, for example, this gap is now mostly about the difference between a farmer’s losses and the payouts that a limited level of affordable coverage can offer.

Only a few years ago, our main worry was that the insurance indexes were not accurately reflecting the severity of a drought, due to things like errors in satellite measurements, or a lack of rain gauges on the ground. Now we are getting to higher accuracy levels, which is great progress, but it leaves less room for solving problems purely through technology.

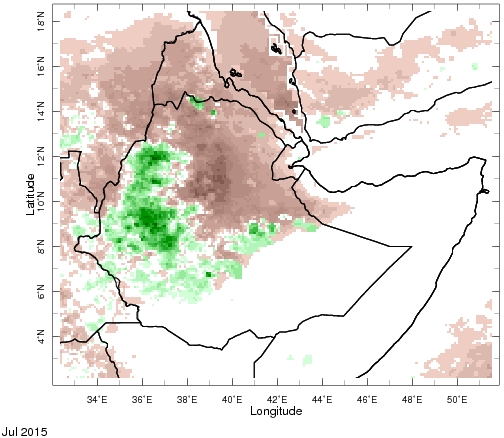

Map shows the extreme rainfall deficits (brown areas) in northern Ethiopia in July 2015, highlighting the early-season drought there.

An example of the high accuracy of the Ethiopia indexes is illustrated in a simple benchmark–how well the index would have covered historical droughts if it had been sold in the past.

Remarkably well, it turns out. The index would have triggered payouts in 7 out of the 9 years the farmers themselves identified during interviews as being the worst in the last three decades.

Of course, interviews about the past are no guarantee of performance in the future, especially since memories can fade. Fortunately, we are also seeing a close connection between the index and what actually happens on the ground as a drought unfolds.

For example, R4 project teams visited about a hundred villages across the area to talk with farmers about the conditions on the ground. We could predict the outcome of the village meeting with about 80% accuracy, simply by using the index. This is about as accurate as science gets, especially when you take into account all the added confusion that village meetings throw in to the mix.

We’re also seeing stronger agreement between different sources of evidence than ever before. When we compare different satellite rainfall estimates, satellite measurements of moisture, satellite proxies of vegetation health, they are in strong agreement. Because these come from different sources, they provide independent sources of evidence. So our confidence in the accuracy is higher, especially since the satellites are saying the same things as rainfall measurements made by the farmers themselves.

We do see room for technical improvement. For example, in 2015 we were testing an additional satellite vegetation component of the index. In 2015 this experimental component performed well, improving the coverage of the overall index to 8 out of the 9 bad years. But these improvements are not giving us the dramatic gains we used to see from working on the technology. We’re already getting most of the years covered.

The larger problem we are facing is that affordable insurance can only have a limited amount of coverage. We are now facing tough choices on where to allocate the coverage. For example, the project has to balance coverage between the beginning of the season and the end of the season. At the beginning of the season, farmers haven’t yet invested a lot of time and money in their crops. They also have non-insurance options, such as re-planting, or planting faster growing, but lower-yield crops. These options disappear by the end of the season. Another challenging trade-off is how much to preserve the coverage for the worst years versus spreading the payouts over more frequent, but less severe years.

In 2015, the insurance was not enough for many farmers to manage the drought. The challenge is that we can only afford to offer partial coverage, and needs often exceed the level of what is covered. Do we sacrifice late season coverage that will clearly be needed in other years to be able provide larger payouts for droughts like the early-season deficit of 2015?

Farmers in Ethiopia have told us during interviews that they wanted the bulk of the coverage targeted to end-of-season droughts, when they are most vulnerable. Even though the massive drought at the beginning 2015 season maxed out the indexes, payouts were limited size because the bulk of the coverage was reserved for late season droughts that fortunately either didn’t occur where there was significant improvements in rainfall, or were not low enough to trigger a payout.

The reality is insurance alone won’t be enough to cover all the risks these farmers face.

R4 solves this problem by using a holistic approach so that the insurance is one part of an integrated toolbox of risk transfer, risk reduction, prudent risk-taking, and risk reserves. In 2015, a special “basis risk” fund was used to fill in the financial coverage needed on top of the insurance payout. This helped bridge the gap between what the insurance could pay and the losses that the farmers experienced, largely due to limited levels of coverage that was very closely targeted to specific components of risk.

This fund has the added benefit of allowing new technologies to be phased in without putting farmers at risk. The fund allowed us to phase in a new satellite vegetation component of the insurance slowly, without having to expose the farmers to an untested product. In 2015, the new index component was a tool to adjudicate the payments of the fund. In 2016, it can be part of the formal insurance product.

But the clear lesson from this year is that technology isn’t the savior. Insurance alone is not enough. Additional coverage comes at an additional price. At a certain point that money is better used for risk management beyond insurance. The payouts can only be part of the solution, even with the perfect insurance product. Models that build micro-insurance projects into a solid risk management package, like R4, are critical.

Dan Osgood is the lead scientist of IRI’s Financial Instruments Sector Team. On twitter, he’s @OsgoodDan.

You must be logged in to post a comment.